308 / 327

308 / 327

308

• Annual Report 2018-19

Shaping the future of software driven business

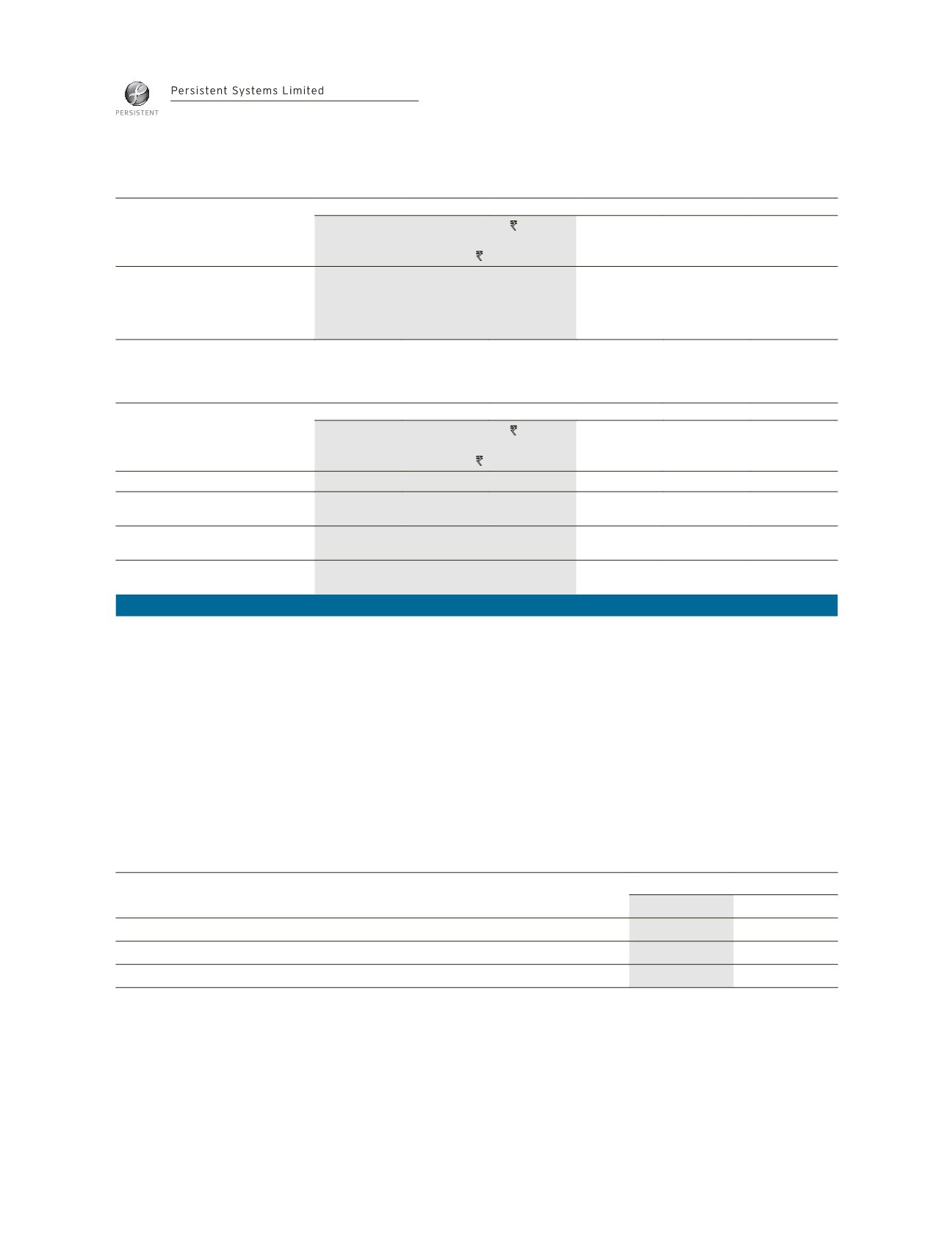

The following table gives details in respect of outstanding foreign currency forward contracts:

As at March 31, 2019

As at March 31, 2018

Foreign

currency

(million)

Average

rate

`

`

(million)

Foreign

currency

(million)

Average

rate

`

`

(million)

Derivatives designated as

cash flow hedges

Forward contracts

USD

112.00

73.00

8,175.45

103.00

66.95

6,895.53

The foreign exchange forward contracts mature within twelve months. The table below analyses the derivative financial

instruments into relevant maturity groupings based on the remaining period as of the balance sheet date:

As at March 31, 2019

As at March 31, 2018

Foreign

currency

(million)

Average

rate

`

`

(million)

Foreign

currency

(million)

Average

rate

`

`

(million)

Not later than 3 months

30.00

69.95

2,098.38

25.00

66.79

1,669.69

Later than 3 months and not

later than 6 months

30.00

74.00

2,220.06

24.00

66.72

1,601.25

Later than 6 months and not

later than 9 months

30.00

74.84

2,245.19

25.00

66.93

1,673.26

Later than 9 months and not

later than 12 months

22.00

73.26

1,611.82

29.00

67.29

1,951.33

Total

112.00

8,175.45

103.00

6,895.53

Credit risk

Credit risk refers to the risk of default on its obligation by the counterparty resulting in a financial loss. The maximum exposure

to the credit risk at the reporting date is primarily from trade receivables amounting to

`

2,429.85 million and

`

3,425.07 million

as at March 31, 2019 and March 31, 2018, respectively. Trade receivables are typically unsecured and are derived from revenue

earned from customers primarily located in the United States. Credit risk is managed by the Company by Credit Task Force

through credit approvals, establishing credit limits and continuously monitoring the recovery status of customers to which

the Company grants credit terms in the normal course of business. On account of adoption of Ind AS 109, the Company uses

expected credit loss model to assess the impairment loss. The Company uses a provisioning policy approved by the Board of

Directors to compute the expected credit loss allowance for trade receivables. The policy takes into account available external

and internal credit risk factors and the Company’s historical experience for customers.

Credit risk is perceived mainly in case of receivables overdue for more than 90 days. The following table gives details of risk

concentration in respect of percentage of receivables overdue for more than 90 days:

As at

March 31, 2019

March 31, 2018

Receivables overdue for more than 90 days (

`

million)*

244.00

410.14

Total receivables (gross) (

`

million)

2,503.51

3,505.27

Overdue for more than 90 days as a % of total receivables

9.7%

11.7%

* Out of this amount,

`

73.66 million (March 31, 2018:

`

80.20 million) have been provided for.

Notes forming part of financial statements (Contd.)